The fastest way to misread b2b payment automation is to treat it as a finance-only upgrade. It’s a systems problem. Orders, invoices, approvals, remittance data, gateway responses, ERP postings, and storefront updates all have to move through clean interfaces without losing context.

That matters because the market is large and still expanding. The global B2B payments transaction market is projected to grow from $1.58 trillion in 2024 to $3.79 trillion by 2034, at a 9.14% CAGR, according to Precedence Research’s B2B payments transaction market forecast. For a SaaS team, that isn’t background noise. It means customers will keep asking for embedded invoicing, approval routing, reconciliation, payout orchestration, and better data sync across commerce and finance systems.

Developers end up owning the hard part. Not the policy. The plumbing.

Why B2B Payment Automation is a Developer Priority in 2026

Finance teams usually describe payment automation in terms of faster approvals and fewer exceptions. Developers see the actual workload: inconsistent schemas, delayed status updates, missing remittance references, race conditions between order events and invoice creation, and brittle connectors to commerce platforms.

That’s why this has become a product priority, not a nice-to-have integration. If your SaaS platform touches orders, fulfillment, ERP sync, receivables, payables, or marketplace operations, customers will eventually expect payment workflows to live inside the product instead of across spreadsheets, inboxes, and bank portals.

The product value sits in the data layer

A useful payment automation feature does three things well:

- Captures financial intent early: the system knows when an order, purchase order, shipment, or approval should create an invoice or payment task.

- Moves status in real time: paid, partially paid, failed, under review, refunded, and reconciled states propagate across systems without manual chasing.

- Preserves context for reconciliation: invoice IDs, order IDs, customer IDs, PO references, tax fields, and payment references stay linked.

This is why payment automation often overlaps with embedded finance. If you’re building native workflows around collections, settlement, or supplier payments, the architecture starts to resemble what product teams discuss in embedded finance platform design.

What works and what breaks

What works is API-first design, event-driven updates, strong idempotency controls, and a clear internal ledger model.

What doesn’t work is bolting a gateway onto a disconnected order system and calling it automation. If invoice generation, payment execution, and reconciliation all happen in different silos, support tickets multiply fast. Customers don’t care which subsystem failed. They care that the order says paid in one place and open in another.

Practical rule: If your team can’t trace one transaction from source order to ledger entry with a single correlation ID, your automation isn’t finished.

Understanding the B2B Payment Automation Ecosystem

B2b payment automation is easiest to understand as a digital logistics network for money and transaction data. Physical logistics moves goods through checkpoints. Payment automation moves records through checkpoints.

The basic objects are familiar to developers: order, invoice, vendor, customer, payment, refund, remittance, settlement, and ledger entry. The challenge is that each object may originate in a different system and arrive on a different schedule.

P2P and O2C in engineering terms

Procure-to-pay (P2P) starts when a company commits to buy. Data usually flows from purchase order to goods receipt to invoice to approval to payment execution to ERP posting.

Order-to-cash (O2C) starts when a company sells. Data flows from order capture to invoice generation to payment request to collection to cash application to reconciliation.

The terms AP and AR sound accounting-heavy, but the engineering tasks are concrete:

- AP automation: ingest supplier invoices, match them against PO and receipt data, route approvals, and trigger payment rails.

- AR automation: generate invoices, collect payments, apply remittances, manage partial payments, and update receivables status.

- Reconciliation: match external money movement to internal financial records and mark the transaction complete.

Why manual workflows still distort system design

A major reason these workflows remain painful is that many companies still run them half-manually. Approximately 51% of companies still perform up to half of their payment operations manually, which drives higher costs, slower cycles, and more errors, as summarized by Zip’s B2B payments statistics roundup.

That manual reality leaks into product requirements. Teams ask for CSV imports because vendor data is inconsistent. They ask for approval overrides because invoice matching fails. They ask for note fields because someone still has to explain payment discrepancies by hand.

Where developers can simplify the ecosystem

A strong implementation usually standardizes around these layers:

- Event ingestion: order placed, invoice received, payment confirmed, refund issued

- Business rules: approval thresholds, due dates, payment scheduling, exception routing

- Execution: gateway calls, bank file handling, notification delivery

- State sync: ERP, commerce platform, CRM, warehouse, and reporting updates

If your customers want to reduce accounts payable costs, the first win usually isn’t fancy AI. It’s replacing fragmented document intake and status chasing with reliable object mapping and event handling.

Manual payment work rarely starts as a finance preference. It usually starts as an integration gap.

Comparing Key B2B Payment Rails and Workflows

Developers don’t choose payment rails based on abstract preference. They choose them based on what the workflow needs: settlement speed, required metadata, reversibility, partner expectations, and how much post-payment reconciliation pain the rail creates.

A common mistake is optimizing only for payment execution. The better approach is to optimize for the full cycle, from invoice creation to ledger close.

What each rail changes in implementation

ACH or bank transfer usually fits recurring domestic B2B flows well. Integration often happens through gateway APIs, bank APIs, or scheduled file exchange depending on the provider. The implementation burden isn’t the debit or credit itself. It’s collecting correct bank details, managing prenotification or verification steps when relevant, and handling delayed confirmation states.

Wire transfer is operationally different. It’s useful when value or urgency justifies more friction. Developers should expect more manual review points, stricter beneficiary data validation, and less forgiving correction paths once the transfer is initiated.

Virtual cards or card-based B2B payments can simplify supplier enablement in some programs because acceptance may already exist. The trade-off is token management, settlement reporting differences, and cases where remittance context is weaker unless your provider returns rich reference data.

Real-time or instant-style payment flows are attractive when confirmation speed matters. They also force better system discipline. You don’t have much room for lagging invoice state or slow downstream consumers when the payment event lands immediately.

Comparison of B2B Payment Rails for Developers

| Payment Rail | Integration Method | Typical Speed | Relative Cost | Data Richness | Best Use Case |

|---|---|---|---|---|---|

| ACH / bank transfer | API integration, bank integration, or file-based processing | Slower than real-time options | Lower | Moderate, depends on remittance quality | Recurring domestic supplier or invoice payments |

| Wire transfer | Bank portal, bank API, or treasury workflow | Faster operational handling | Higher | Moderate | High-value or urgent payments |

| Virtual card | Gateway or issuer API | Fast authorization workflow | Variable | Moderate to strong when provider returns detailed transaction data | Controlled supplier spend and AP programs |

| Card payment portal | Hosted payment page or gateway API | Immediate customer action | Variable | Strong for user-facing payment status | AR collections and self-service buyer payments |

| Real-time payment flow | API-first provider integration | Immediate or near-immediate confirmation | Variable | Good when reference data is enforced | Urgent collections and instant settlement use cases |

The trade-offs teams miss

The wrong rail usually reveals itself during reconciliation, not checkout or payout.

For invoice-heavy operations, the decision should consider:

- Reference quality: Can you reliably pass invoice number, PO number, customer ID, and internal transaction ID?

- Failure semantics: Do you get synchronous rejection, asynchronous failure, or silent delay?

- Partial payment handling: Can the rail support split settlement cleanly in your internal model?

- Return path: What happens when a payment must be reversed, disputed, or reissued?

Teams building AP workflows often benefit from a separate design review focused on invoice ingestion and approvals before selecting rails. This guide for accounts payable automation is useful because it frames the upstream invoice problem that often determines downstream payment complexity.

For platforms that also need marketplace or sub-merchant payout patterns, it helps to understand how Stripe Connect structures connected account flows. Even if you don’t use that stack, the architectural patterns are relevant.

Choose the rail that minimizes exception handling for your dominant transaction type, not the rail with the cleanest demo.

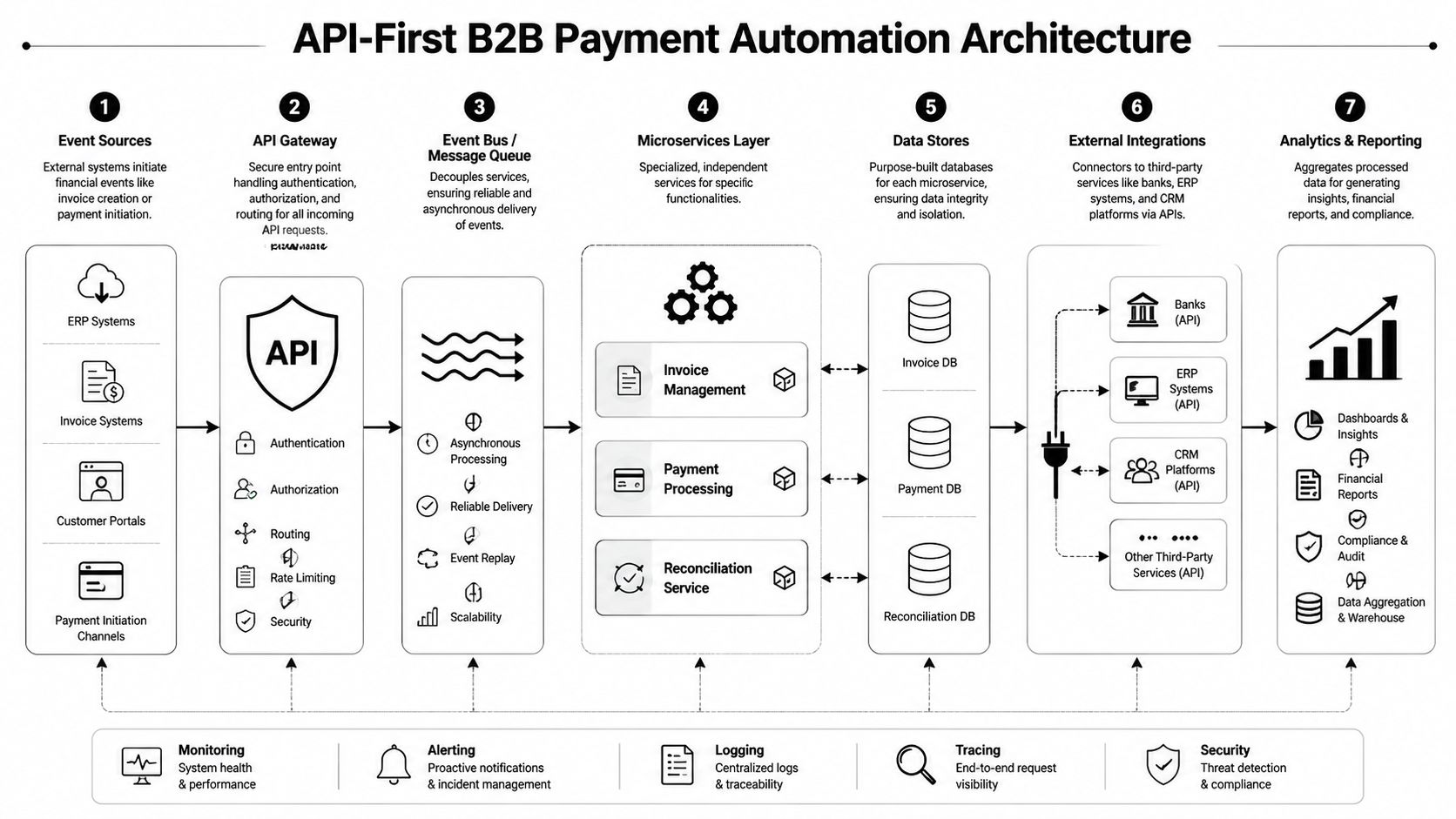

Technical Architecture and API Integration Patterns

The strongest payment automation systems are API-first and event-driven. They don’t wait for finance staff to reconcile statuses manually, and they don’t depend on nightly sync as the primary truth model.

The core pattern is simple. External systems emit events. Your platform normalizes those events. Internal services decide what to do next, then push updates outward to gateways, ERPs, and commerce systems.

Webhooks first, polling when necessary

Webhooks should be your default for payment-state changes, invoice lifecycle updates, and order events where latency matters. They reduce lag and avoid wasteful polling loops.

Polling still has a place. Some systems don’t support webhooks. Others expose them inconsistently. In those cases, date-filtered list endpoints and checkpoint-based sync can be reliable if you build proper deduplication and replay logic.

A practical architecture often includes:

- API gateway: authentication, rate limiting, request validation

- Event bus or queue: decouples ingestion from processing

- Invoice service: generation, validation, status model

- Payment orchestration service: gateway interaction, retries, scheduling

- Reconciliation service: remittance parsing, ledger posting, exception management

- Audit store: immutable trail for support and compliance review

A concrete order-to-cash flow

A realistic O2C sequence for a SaaS platform looks like this:

- Order event arrives from a commerce platform or ERP.

- Normalization layer maps external order data to your internal schema.

- Invoice service creates an invoice record with due date, line items, tax, customer ID, and references.

- Payment instruction is scheduled based on terms, payment method, or buyer portal action.

- Gateway response updates transaction state.

- Confirmation event triggers cash application and ledger sync.

- Status sync updates the source commerce or ERP system.

This pattern gets much stronger when matching logic is automated. According to Tipalti’s overview of B2B payments automation, API-driven real-time data exchange combined with RPA can reduce invoice processing errors by up to 80% and accelerate cycle times from days to hours, and some systems use APIs to perform 3/4-way PO matching with 99% accuracy.

Design choices that hold up in production

Developers should be opinionated about a few things:

- Use idempotency keys for all payment initiation calls.

- Store raw payloads alongside normalized objects for traceability.

- Version your mapping layer because upstream schemas will change.

- Separate payment intent from payment settlement in your data model.

- Build exception queues for unmatched remittances and disputed invoices.

If you’re working with bank and payment data aggregation patterns, the broader open banking API model is worth understanding because it influences consent flows, account data retrieval, and payment initiation design.

Solving eCommerce Connectivity for Payment Automation

Payment automation gets much harder when your customers sell through multiple commerce systems. One merchant uses Shopify, another runs Adobe Commerce, another mixes WooCommerce with Amazon and Walmart, and all of them expect the same clean invoice and payment workflow inside your SaaS product.

Many roadmaps often break at this stage. The payment logic may be sound, but the source data is fragmented across cart APIs, marketplace APIs, different auth models, and inconsistent event support.

The connectivity problem from a developer’s desk

A 2023 survey noted that 58% of businesses see integration as a growing trend, yet developers still struggle to connect payment systems to more than 70 eCommerce carts. Unified APIs such as API2Cart can reduce engineering costs by up to 9x and provide a single integration point for real-time payment data sync, according to American Express’s article on how automation can transform B2B payments.

That matters because payment automation depends on upstream commerce signals:

- new order created

- order updated

- shipment completed

- refund issued

- customer record changed

- payment status changed on the sales channel

If you build separate connectors for each platform, maintenance becomes the hidden cost center. Every connector needs schema mapping, auth handling, pagination logic, webhook support, changelog monitoring, and regression testing.

A cleaner order-to-cash pattern

For OMS, ERP, WMS, and accounting vendors, the practical pattern is:

- Pull or receive new orders from connected stores through one normalized integration layer.

- Map orders into your internal invoice model.

- Trigger the payment or receivables workflow.

- Write paid, partially paid, or refunded status back to the original sales channel.

- Keep customer and shipment context attached for support and reconciliation.

This becomes even more important for teams that also support region-specific bank flows. If your stack includes bank file handling in Europe, this resource on handling SEPA files with payment gateways is helpful because it shows where gateway orchestration and banking formats intersect.

The fastest way to make payment automation brittle is to treat commerce connectivity as a separate project. It isn’t. It’s the source of truth for half the workflow.

What usually fails

Three patterns fail repeatedly:

- Over-customized mappings: every merchant gets unique field logic with no reusable transformation layer.

- No replay strategy: webhook outages create permanent gaps in order or payment state.

- One-way sync: your system imports order data but never pushes financial state back to the channel.

Developers should insist on bidirectional sync. Otherwise support teams end up reconciling truth manually between storefront, ERP, and payment system.

Your Phased Roadmap for Implementing Payment Automation

Organizations shouldn’t try to automate everything at once. The better rollout is phased, with each phase producing a stable internal capability before the next one depends on it.

Phase one builds the transaction backbone

Start with normalized data ingestion and canonical objects.

Your platform needs stable internal models for customer, order, invoice, payment instruction, remittance, and ledger event. If those objects are weak, every later automation feature becomes exception-driven.

Focus on these deliverables first:

- Canonical schema: one internal representation regardless of source platform

- Event capture: webhook ingestion where available, polling fallback where needed

- Reference discipline: invoice IDs, order IDs, external IDs, and customer IDs must remain linked

- Auditability: raw payload storage plus transformed records

Don’t start with “smart” approvals or AI matching if your incoming records don’t normalize cleanly.

Phase two handles payment execution safely

Once invoices and payable or receivable states are reliable, connect the payment layer. Keep the execution service narrow. It should accept validated instructions, call the provider, persist responses, and emit status events.

At this stage, security controls stop being optional engineering debt and become release criteria. According to Invoiced’s B2B payment automation guidance, advanced systems using AI-powered cash application and multi-channel dunning can achieve over 90% auto-match rates for remittances and must adhere to AES-256 encryption and SOC 2 compliance, while connecting to ERPs and eCommerce platforms via RESTful APIs with OAuth2.

That translates into concrete developer tasks:

- Tokenize sensitive payment details instead of storing raw account or card data

- Encrypt data at rest and in transit

- Use scoped OAuth2 access for external integrations

- Separate duties in admin tooling so operational overrides are auditable

Phase three automates reconciliation and collections

At this stage, teams usually discover whether the product offers actual utility.

Once payment confirmations arrive, your system should apply cash automatically whenever confidence is high and route the rest to an exception queue with context attached. For AR-heavy products, add dunning flows only after payment matching is stable. Bad reminder logic on top of bad matching creates customer-facing mistakes.

A production-ready reconciliation layer should support:

- Exact-match application when invoice number and amount align.

- Tolerant matching for partial payments, short pays, and bundled remittances.

- Human review queues with raw bank and remittance data visible.

- ERP posting rules that don’t require manual spreadsheet cleanup.

Implementation note: Security work belongs inside each phase. If you defer encryption, tokenization, audit logging, and access control until the end, the release will stall.

Choosing a Payment Partner and Measuring ROI

The right payment partner makes the integration easier to operate, not just easier to demo.

Developers should screen vendors with a technical checklist before procurement gets too far:

- API quality: clear object models, predictable errors, versioning policy, and webhook documentation

- Sandbox realism: test environments should simulate asynchronous states, failures, and retries

- Operational tooling: event logs, replay controls, idempotency support, and searchable transaction history

- Security posture: tokenization support, modern auth, encryption standards, and audit features

- Data return quality: settlement details and remittance references must be usable for reconciliation

Pricing matters, but unclear event semantics usually cost more than higher transaction fees.

The KPIs that actually prove value

For product and engineering teams, ROI should be measured through system outcomes, not vague automation language.

Track:

- Invoice processing time

- Payment error rate

- Auto-reconciliation rate

- Exception queue volume

- Time to resolve unmatched payments

- Sync consistency across commerce, ERP, and payment systems

The best result isn’t just lower manual effort. It’s fewer places where humans need to guess what happened.

If your SaaS product depends on multi-channel commerce data, payment automation only works as well as your integrations do. API2Cart gives development teams a unified way to connect with 70 shopping carts and marketplaces, so you can build order-to-cash and payment sync features without maintaining dozens of custom connectors. It’s a practical option for validating workflows faster, reducing integration overhead, and shipping payment-aware commerce features sooner.