Embedded finance stopped being a side topic for product teams once it became clear that users don’t want to leave the workflow to pay, borrow, insure, or get paid. They want financial actions inside the software they already use.

For B2B eCommerce SaaS teams, that changes the build agenda. “What is embedded finance” is no longer just a definitional question. It’s a platform question. If your product touches orders, inventory, customer records, shipments, or marketplace operations, you already sit near the data needed to power financial decisions. The hard part isn’t inventing a use case. The hard part is delivering it across fragmented cart and marketplace ecosystems without creating an integration maintenance mess.

The Embedded Finance Boom Why SaaS Developers Must Pay Attention

The market size alone should reset how teams think about this category. The global embedded finance market was valued at USD 104.8 billion in 2024 and is projected to reach USD 834.1 billion by 2034, with a projected 23.3% CAGR from 2025 to 2034, according to Global Market Insights.

That projection matters because it tells developers something practical. Financial features are moving from “nice to have” add-ons into baseline product capabilities across software categories that historically had nothing to do with banking.

What this means in a SaaS product roadmap

For a B2B SaaS vendor, embedded finance means putting a financial action inside an existing product flow instead of sending the user to a separate financial provider.

That can mean:

- At checkout: offering payment options directly in the cart flow

- Inside an OMS: surfacing merchant financing based on order behavior

- In a shipping platform: attaching shipment protection when labels are created

- Within an ERP or PIM: offering payment terms, trade credit, or invoice-linked financing

The opportunity is obvious. The implementation is not.

The eCommerce problem most articles skip

Most embedded finance explainers focus on consumer apps. They talk about ride sharing, food delivery, or digital wallets. That’s useful background, but it doesn’t answer the question an integration developer has to solve:

How do you deliver one finance feature consistently across Shopify, WooCommerce, Amazon, eBay, Walmart, and every other store system your customers already use?

That’s the fundamental issue in B2B eCommerce software. A finance feature is only as good as the data behind it. If eligibility depends on order history, refund behavior, inventory levels, shipment events, or customer records, then fragmented cart connectivity becomes the bottleneck.

What works is treating embedded finance as an integration architecture problem first and a feature problem second.

What doesn’t work is bolting a lending or payments API onto a product without planning how order and customer data will be normalized across carts. Teams that skip that step usually end up with inconsistent behavior by platform, brittle edge-case handling, and support tickets tied to connector drift rather than finance logic.

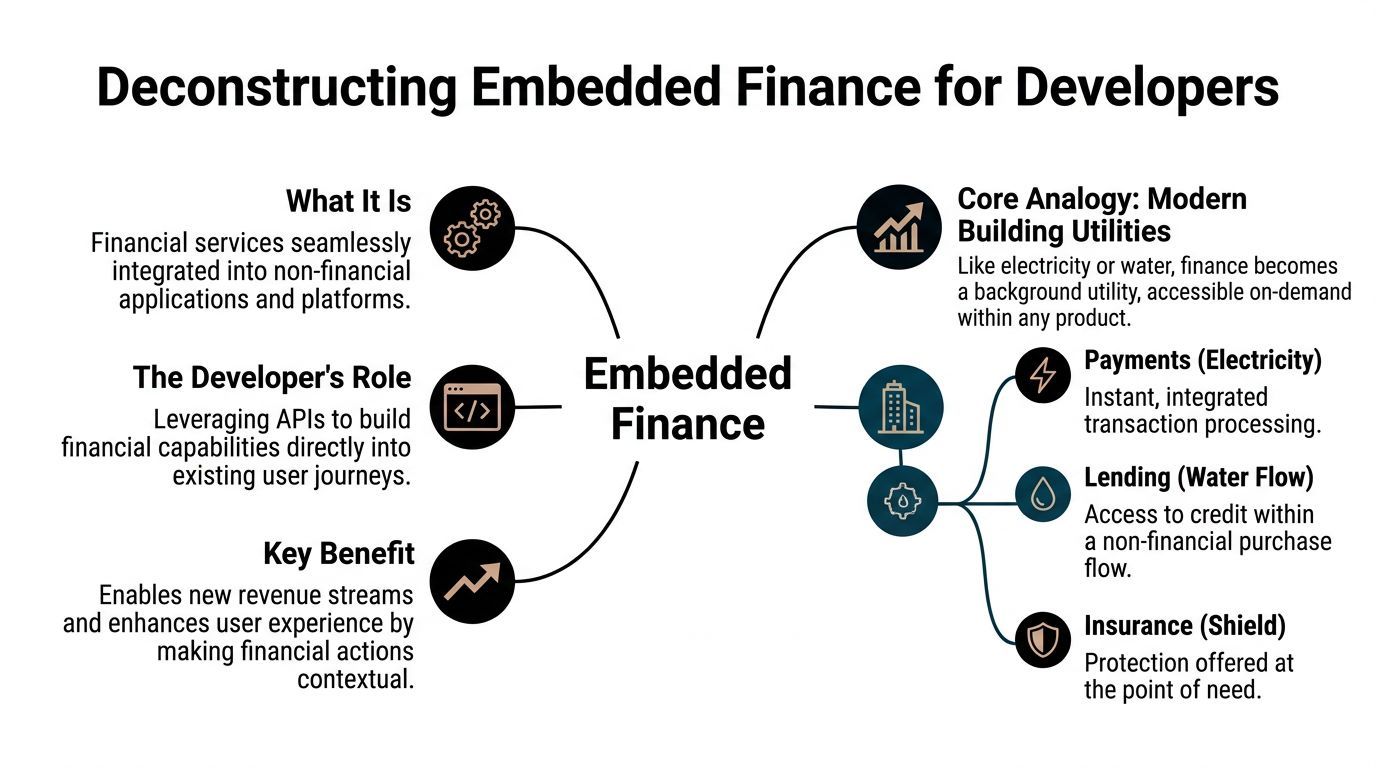

Deconstructing Embedded Finance What It Means for Developers

A clean way to think about embedded finance is this: it makes money movement and financial products behave like built-in product utilities.

Users don’t want to see the plumbing. They want the tap to work.

The utility model

In a modern building, nobody asks where the water pressure is managed or how the electrical routing reaches each floor. Those systems are expected to be present, safe, and available when needed.

Embedded finance works the same way inside software:

- Payments become part of checkout or invoice settlement

- Lending appears at the point where the buyer or merchant needs liquidity

- Insurance shows up when shipment or product risk is present

- Payouts happen within the platform that already manages the commercial workflow

From a product perspective, the user experiences a smoother flow. From a developer perspective, that smoothness hides a stack of regulated infrastructure, partner APIs, data models, event handling, and compliance controls.

The three-layer model developers should use

Teams often understand embedded finance faster when they separate the stack into actors:

| Layer | Who owns it | What they do |

|---|---|---|

| Experience layer | SaaS platform | Embeds the financial action into the user journey |

| Enablement layer | BaaS or fintech infrastructure provider | Exposes APIs, orchestration, and operational capabilities |

| Regulated layer | Licensed financial institution | Holds the regulated permissions and access to financial rails |

That structure matters because your SaaS company usually doesn’t need to become a bank. It needs to integrate with providers that already operate the regulated layer and expose controlled capabilities through APIs.

Practical rule: If your team is asking whether you need to “build banking,” you’re usually asking the wrong question. The right question is which capabilities belong in your product layer and which belong to regulated partners.

Where developers fit

The developer’s role is not to replicate a bank core. It’s to build a dependable orchestration layer between the product workflow, the commerce data, and the finance provider.

That means:

- defining the events that trigger finance logic

- mapping cart and marketplace data into a stable internal model

- passing only the right data to partners

- handling asynchronous outcomes such as approvals, declines, settlements, and returns

- keeping the user experience coherent when third-party systems respond late or differently than expected

Teams building in this space often benefit from broader reading on fintech software development, especially around how product engineering changes once financial services become part of the application boundary.

What is embedded finance in practical terms, then? It’s API-delivered financial capability inside a non-financial product, but for developers its actual meaning is narrower and more useful: it’s a distributed system problem with money, compliance, and user trust attached.

Core Components and Business Models

Embedded finance is not one product. It’s a family of product patterns that attach financial capability to a commercial moment.

Investor activity shows why teams keep moving into the space. Venture capital investment in embedded finance startups hit $4.2 billion in Q1 2025 alone, and Affirm reported 24% growth in active consumers to 23 million plus a $52 million net profit turnaround by mid-2025, according to Open Ledger.

The four product families

Embedded payments

This is the most familiar category. The software platform lets users pay without leaving the workflow.

For an eCommerce SaaS team, payments are often the first finance feature because the user expectation is already there. The trade-off is that payment UX looks simple while failure handling, refunds, reconciliation, and platform variance are not.

Embedded lending

Many B2B SaaS products become more compelling. Lending can include BNPL at checkout, merchant cash advances, inventory-linked financing, or invoice-based funding.

A lending feature only works if the underlying operational data is current and trustworthy. If order volume, returns, cancellations, or shipment delays are stale, the finance logic will be wrong.

Embedded insurance

Insurance fits naturally into commerce events because risk already exists in the transaction. Shipping protection, warranty add-ons, or seller protection are common patterns.

This category is often easier for product teams to explain internally because the user need is visible at the moment of purchase or fulfillment.

Embedded investments and treasury-like features

This is less common in standard eCommerce SaaS, but it appears in platforms that handle balances, payouts, or retained merchant funds. It usually comes later because the operational and regulatory model is more demanding.

How SaaS vendors make money

The revenue model depends on the product and partner setup. The common structures are:

- Revenue share on finance activity: A partner handles the regulated side and shares part of fees or finance income.

- Payment-related economics: Teams monetize transaction activity where the commercial model allows it.

- Higher-tier SaaS packaging: Financial workflows become part of premium plans because they change the product’s economic value, not just its feature list.

A useful adjacent example appears in products built around automated invoice processing software. Once invoice capture, approval, and payment timing live in one workflow, finance features become easier to attach because the product already controls key commercial steps.

What works and what doesn’t

What works:

- attach the product to a clear operational event

- pick one revenue logic before expanding the catalog

- launch with a narrow user segment that has predictable workflow patterns

What doesn’t:

- adding multiple finance products at once

- treating approval logic as a black box with no internal observability

- assuming every cart or marketplace exposes the same payment-relevant fields

The commercial side of API-led platform building is well illustrated in this discussion of the eCommerce API economy business model, where the integration layer itself becomes part of the product’s monetization strategy.

Technical and Operational Integration Requirements

Once a team moves past the product idea, architecture becomes the deciding factor. Embedded finance punishes shortcuts because latency, state changes, and external dependencies all show up in the same workflow.

Enterprise-grade embedded finance platforms use microservices deployed via Docker and Kubernetes, and a major infrastructure decision is whether payment origination reaches the network through direct Federal Reserve connectivity or through intermediary processors. Direct connectivity provides operational detail such as IMADs and real-time settlement timestamps, according to ITMAGINATION’s guide to embedded finance architecture.

Why microservices matter here

A monolith can handle a prototype. It becomes painful once finance workflows start scaling unevenly.

Eligibility checks, payment orchestration, ledger updates, notifications, and reconciliation do not have the same load profile. They also don’t fail the same way. Microservices let teams scale and isolate those functions independently.

That matters in eCommerce because a cart import spike, a marketplace sync delay, and a payment status callback can all hit the system at the same time.

If one service processes offers and another tracks settlements, they shouldn’t force each other into the same deployment cadence.

The minimum integration stack

A practical embedded finance stack usually includes these pieces:

- API gateway for routing, authentication, throttling, and policy enforcement

- Identity and access controls for merchant, admin, and partner scopes

- Event pipeline for order creation, shipment updates, cancellations, returns, and payment state changes

- Normalized internal data model spanning customers, orders, products, offers, and payment objects

- Observability layer covering request tracing, async job health, and partner callback outcomes

- Sandbox environment for testing partner flows without contaminating production records

Many teams also need a sponsor bank or equivalent regulated partner relationship in the background, depending on the specific finance service being offered.

Data orchestration is where projects usually get stuck

The technical challenge isn’t only calling a finance API. It’s assembling consistent input from systems that disagree about structure and timing.

A lending decision may need:

| Input | Why it matters |

|---|---|

| Order history | Indicates commercial activity over time |

| Inventory state | Supports stock-aware finance logic |

| Shipment events | Helps distinguish active demand from stalled fulfillment |

| Customer records | Ties buying behavior to entity history |

| Refund and cancellation signals | Prevents overestimating stable revenue |

If those inputs arrive in different formats across carts, you need translation logic before you can build finance logic.

Teams dealing with distributed integrations often run into the same issue described in broader SaaS integration patterns. The system boundary keeps expanding, but the user expects one coherent outcome.

The architecture choices that age well

The designs that hold up tend to share a few traits:

- Event-first thinking: treat finance triggers as state changes, not page actions

- Idempotent processing: retries are normal in payment and marketplace systems

- Clear fallback paths: if a partner response is delayed, the user still needs a sane status

- Strong contract boundaries: keep cart-specific fields out of the core finance domain when possible

What fails over time is tightly coupling finance logic to each connector. That creates a slow-moving system where every new cart or marketplace adds risk to regulated workflows.

Embedded Finance in B2B eCommerce A Goldmine for SaaS

The most overlooked embedded finance opportunities sit inside B2B eCommerce software, not consumer apps. The pattern is simple. Commerce software already sees the operational signals that financial products need.

The challenge is the connector layer. The primary unaddressed issue is embedded finance across multi-cart marketplaces, where B2B SaaS vendors try to support services like BNPL across 70+ carts such as Shopify and Amazon while serving 1M+ merchants, as noted by TreviPay’s discussion of embedded finance and its gaps.

Practical use cases by product type

OMS platforms

An order management system has visibility into order volume, returns, fulfillment timing, and channel spread. That creates a credible basis for finance triggers.

A practical use case is inventory-backed or sales-linked financing offered to merchants when order flow suggests near-term working capital pressure.

PIM and catalog systems

A PIM sits close to product availability, pricing, and channel merchandising. That makes it useful for finance-adjacent decisions, especially in B2B wholesale contexts.

A PIM-driven workflow can support dynamic payment terms tied to product class, margin profile, or buyer segment.

Shipping and fulfillment platforms

Shipping software already knows when a parcel enters risk. Embedded insurance makes sense here because the value proposition aligns directly with fulfillment events.

This is one of the cleaner embedded finance patterns because the trigger is operationally obvious.

ERP and back-office tools

ERP systems hold invoice state, customer terms, and reconciliation data. That makes them strong candidates for embedded payments and financing workflows tied to receivables.

Why multi-cart support changes everything

A finance feature that works beautifully on one platform can become inconsistent across a broader merchant base.

Common reasons:

- Field mismatch: order, tax, or customer schemas differ by platform

- Event timing drift: one platform pushes updates, another requires polling

- Capability gaps: some carts expose rich shipment events, others don’t

- Marketplace edge cases: channel-owned buyer data may be limited or delayed

The finance logic is rarely the first thing that breaks. The input assumptions break first.

That’s why teams should treat data normalization as the first embedded finance milestone. If the same merchant behavior produces different risk or payment outcomes depending on cart source, users lose trust quickly.

The winning pattern

The strongest B2B SaaS teams don’t start by asking which financial product to launch first. They start by asking which commerce events they can observe reliably across their supported platforms.

That approach usually leads to better sequencing:

- unify order and customer visibility

- normalize event timing

- add one finance workflow tied to one operational trigger

- expand only after the cross-platform behavior is stable

In eCommerce SaaS, embedded finance becomes valuable when it is boringly reliable. Novelty gets attention. Consistency keeps merchants using it.

The API2Cart Advantage Accelerating Your Finance Strategy

A BaaS or fintech provider can expose the financial capability. That still leaves a major gap. Your application needs normalized commerce data before it can make or trigger a financial decision.

A unified abstraction layer is key. API2Cart’s unified API approach is built for teams that need one integration surface across many carts and marketplaces instead of maintaining platform-specific connectors individually.

Where it fits in an embedded finance stack

For an integration developer, the value is straightforward:

- One API surface for many platforms: the product team works against a stable interface instead of cart-specific implementations

- Access to operational entities: orders, products, customers, shipments, inventory, and catalogs can feed finance logic

- Webhook support where available: useful for triggering offers or payment-adjacent actions when commerce events happen

- Polling fallback with date filters: important where real-time event support varies by platform

- Broad method coverage: enough retrieval and management depth to support underwriting inputs, reconciliation context, and workflow automation

What that changes in practice

Without a unified commerce data layer, teams often spend most of the project on connector maintenance rather than finance capability.

With a normalized approach, developers can focus on the parts that actually differentiate the product:

- eligibility rules

- offer presentation

- exception handling

- merchant admin controls

- auditability

- partner coordination

That shift matters because embedded finance projects fail when too much engineering time disappears into platform-by-platform data cleanup.

The practical lesson is simple. If your product serves multiple carts or marketplaces, embedded finance starts with reliable access to commerce data at scale. Everything else sits on top of that.

“Frictionless” is the wrong mental model if it causes teams to ignore compliance boundaries. Embedded finance can feel smooth to the user while still demanding strict controls under the hood.

A major blind spot for B2B SaaS teams is cross-marketplace compliance design. Upcoming EU PSD3 requirements effective in 2026 mandate unified identity verification, and fragmented compliance systems are projected to increase costs by 25%, according to PwC’s analysis of embedded finance complexity.

The guardrails developers should assume from day one

- KYC and AML are shared responsibilities: a partner may run regulated checks, but your product still controls data collection paths and user actions

- Data minimization matters: send only what the finance flow needs

- Auditability matters more than elegance: every approval, decline, override, and retry should be traceable

- Jurisdiction differences matter: a workflow that is acceptable in one market may need identity, consent, or disclosure changes in another

A sensible starting point is narrow. Pick one use case, define the event model, map the required data, and validate compliance assumptions with partners before writing production-grade orchestration.

What is embedded finance in the end? For a B2B eCommerce SaaS team, it’s a business opportunity built on APIs, operational data, and careful systems design. Teams that solve the integration layer first usually move faster and break less.

If you’re exploring embedded payments, lending, or insurance inside an eCommerce SaaS product, start with the data layer. API2Cart gives development teams a single way to work with orders, products, customers, shipments, and inventory across many carts and marketplaces, which makes it easier to prototype and validate embedded finance workflows without building dozens of separate connectors first.