The queue usually looks the same. One customer wants orders pushed into accounting as invoices. Another needs refunds split correctly across payment, tax, and shipping lines. A third wants marketplace settlements matched to payouts. Meanwhile, engineering is staring at five different cart schemas, inconsistent webhook behavior, and a finance team that won't accept “close enough” totals.

That's where finance system integration gets real for eCommerce SaaS.

For developers, this isn't a vague digital transformation project. It's the work of turning store activity into financially usable records. Orders, refunds, taxes, discounts, fees, customers, shipping charges, and payout references all have to move from commerce systems into accounting, ERP, billing, or reporting workflows without breaking auditability on the way.

The challenge isn't just getting data out of a cart API. The hard part is making that data trustworthy enough for finance operations. A sync that imports orders but misses partial refunds, tax adjustments, or fee allocations creates more work than it removes. That's why the integration architecture matters as much as the endpoint coverage.

Why Finance System Integration Is Critical for eCommerce SaaS

A merchant-facing SaaS product starts to feel incomplete the moment finance data has to be exported by hand. If your users sell across storefronts or marketplaces, they don't want CSV gymnastics when compiling financial records. They want clean financial records generated from commerce events as they happen.

In practice, finance system integration for eCommerce means connecting store data to downstream finance workflows. The data path usually includes some mix of orders, line items, taxes, refunds, shipping charges, transaction status, customer records, and product metadata. The destination can be an accounting system, ERP, analytics layer, or an internal ledger service that standardizes records before posting them elsewhere.

The broader market pressure is clear. The global data integration market is projected to grow from $15.24 billion in 2026 to $47.60 billion by 2034, while 95% of IT leaders identify integration as a primary barrier to AI adoption and only 28% of enterprise applications are connected, according to Integrate.io's analysis of enterprise data integration adoption. For an eCommerce SaaS team, that gap shows up as product backlog, support tickets, and brittle manual workarounds.

Where eCommerce finance flows usually break

Most failures happen in the translation layer between commerce and finance.

- Order structure mismatch. A storefront sends one order object, but finance needs separate treatment for revenue, tax, shipping, discount, and payment timing.

- Refund ambiguity. Partial refunds rarely map cleanly unless you preserve item-level and tax-level context.

- Fee blindness. Marketplace and payment fees often arrive on a different timeline than the originating order.

- Timing conflicts. The order date, payment capture date, fulfillment date, and settlement date may all be different.

Practical rule: If the integration can't explain how an order becomes a journal-ready record, it isn't finished.

That's why developers need to think beyond raw connectivity. Finance integration succeeds when the data is normalized, timed correctly, and reconciled against business rules.

For teams that are also cleaning up payables and approval workflows on the finance side, Steingard Financial's guide to AP automation is a useful companion read because it highlights the operational cost of leaving finance processes dependent on manual handoffs.

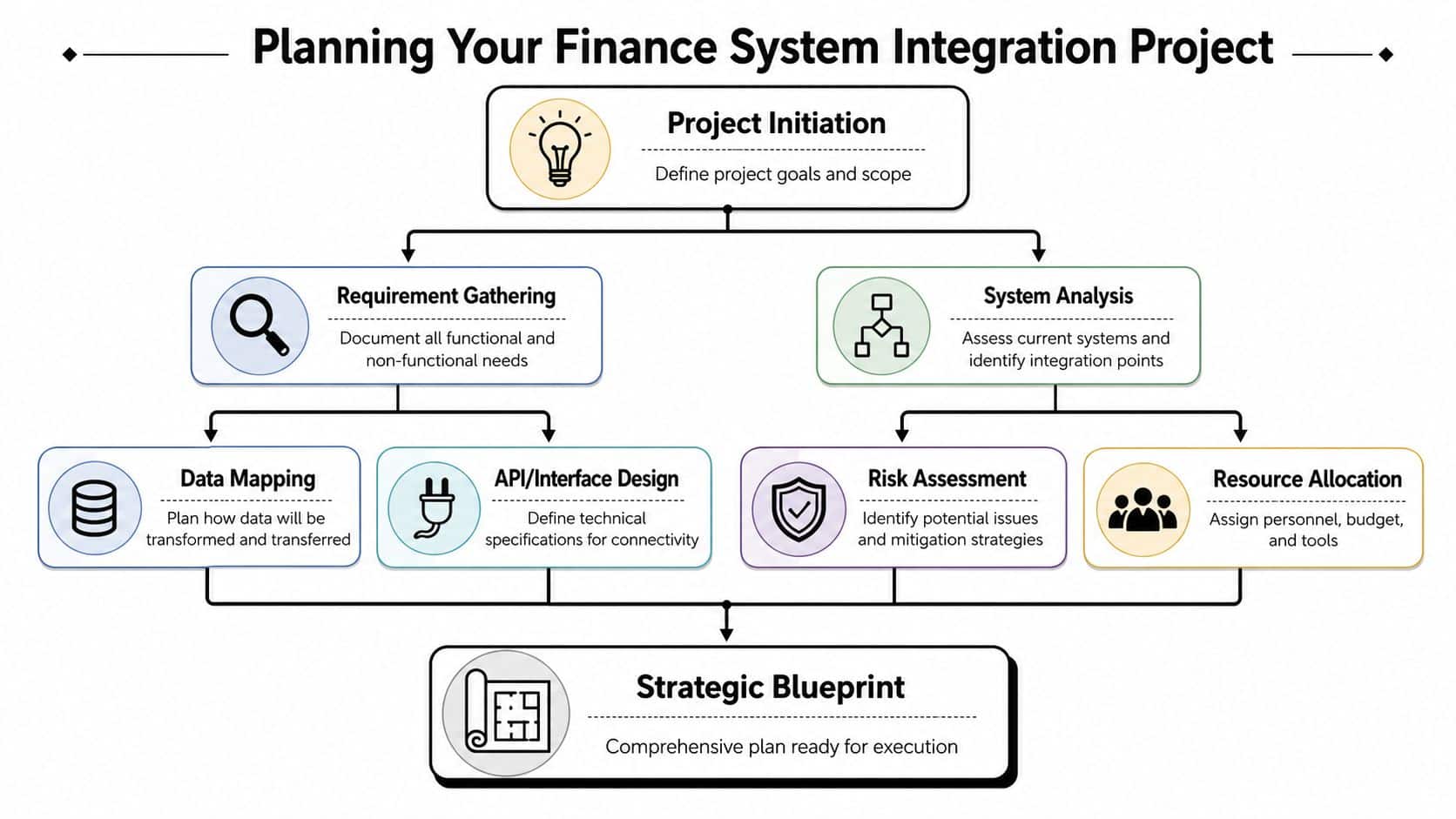

Planning Your Finance System Integration Project

The first bad decision in these projects is usually made before development starts. Teams say they're integrating “orders into accounting,” but they haven't defined what counts as an order for finance purposes. That's how projects drift into edge-case chaos.

A workable plan starts with the future-state operating model. That phased approach matters. Guidance from the IMAA Institute on executing finance integration strategy recommends defining the future-state model, assessing ownership, establishing Day One must-haves, and then moving into implementation with detailed IT milestones. It also notes that milestones are more likely to be met when they're distributed across workstreams instead of packed into a single cutover.

Define the finance events first

Start with the records finance needs, not the API objects the store happens to provide.

A typical commerce-to-finance flow needs answers to questions like these:

- Is an order posted at creation, payment capture, fulfillment, or settlement?

- Are discounts allocated by line, proportionally, or as a separate negative line?

- Do taxes post per line, per jurisdiction summary, or as a single order-level amount?

- How are shipping charges handled?

- What happens when a refund is partial, delayed, or split across items?

Those decisions shape the mapping model.

Data mapping is where most of the work lives

A multi-line order looks simple in a storefront response and messy in finance.

Take a common case. One order contains multiple items, an order-level discount, shipping, tax, and a later partial refund against only one line. Finance usually can't accept that as one blob. It needs structured entries that preserve source references and support later reversals. That means you need deterministic mapping rules for:

- Revenue allocation across line items

- Discount treatment at order or item level

- Tax handling when the source system mixes inclusive and exclusive tax models

- Refund logic that reverses only the affected portions

- Fees and settlement references if payouts are tracked separately

The integration should preserve enough source detail to reproduce the financial outcome later. If you flatten too early, reconciliation gets harder fast.

Developers often underestimate this layer because endpoint access feels like progress. It isn't. Mapping rules, idempotency keys, status transitions, and exception handling are what make the integration usable.

Build every connector or standardize the input

If you support many storefronts, bespoke connectors become a maintenance liability. Every cart has different field names, pagination behavior, webhook coverage, and order semantics. You don't just build once. You inherit version drift and edge-case support work.

That's why many teams look for a normalized access layer instead of writing and maintaining cart-specific connectors. For product teams working through ERP-side requirements, Grumspot's Shopify ERP solutions is a useful reference on the operational side of that bridge. On the API abstraction side, API2Cart's coverage for Sage Intacct integration scenarios shows the kind of unified commerce-data access model developers often use to reduce connector sprawl.

A good planning boundary is simple:

| Decision area | Define before coding |

|---|---|

| Source systems | Which carts, marketplaces, and payment-related records are in scope |

| Finance outputs | Invoice, journal, payout, settlement, or reporting record |

| Trigger points | Order create, paid, shipped, refunded, settled |

| Ownership | Product, engineering, finance ops, support |

| Failure path | Retry, hold, alert, or manual review |

If those answers are fuzzy, the implementation will be fuzzy too.

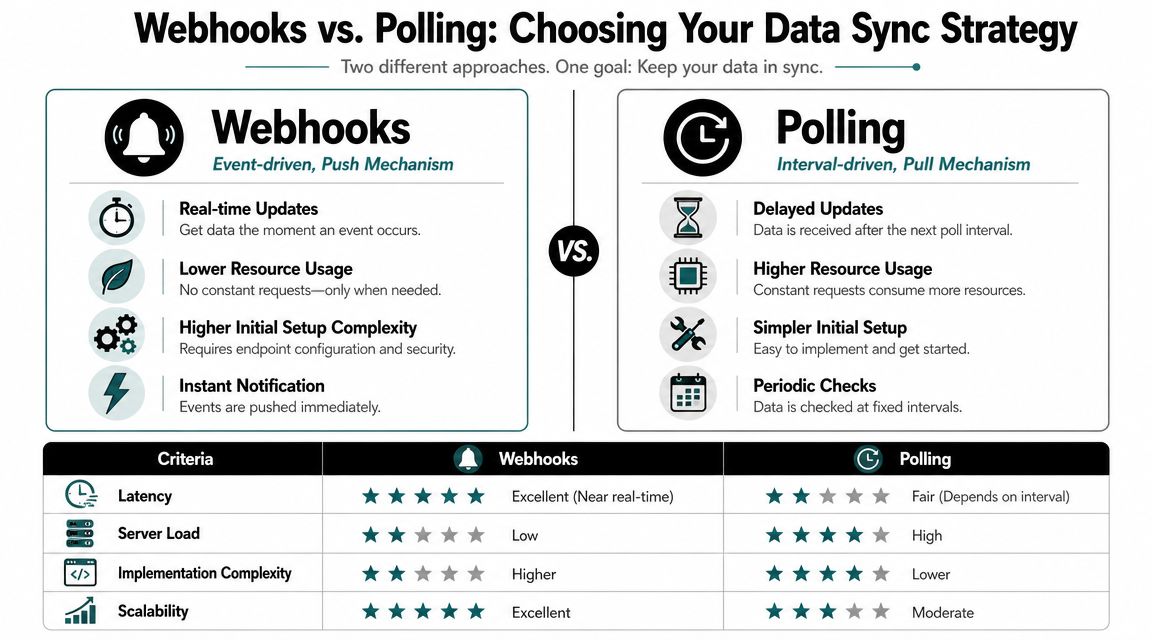

Choosing Your Data Sync Strategy Webhooks vs Polling

The sync pattern changes the quality of the whole integration. It affects latency, infrastructure load, retry design, and how quickly finance records reflect store activity.

Organizations often choose between polling and webhooks. The right answer usually isn't one or the other. It's a deliberate mix.

Polling works when consistency matters more than immediacy

Polling is the pull model. Your service asks the source system for changes on a schedule, usually with updated-at filters, pagination, and retry control. It's straightforward to implement because your side controls the loop.

For finance workflows, polling is often the safer baseline when you need repeatable retrieval logic for records such as newly updated orders, refunds, or shipment-linked status changes. A common implementation pattern is querying order lists by last-modified window, then reprocessing any records whose state changed since the previous checkpoint.

Polling is especially useful for:

- Backfill jobs that import historical orders

- Reconciliation sweeps that confirm no records were missed

- Systems with weak event coverage where not every finance-relevant event produces a push notification

- Controlled retry windows for delayed or eventually consistent source data

The downside is obvious. Polling introduces latency, increases request volume, and can run into source-side rate limits if you aren't careful with date filters and page sizes.

Webhooks work when timing matters

Webhooks are the push model. The source sends your application an event when something happens. For finance integration, that's attractive when a new paid order, cancellation, or refund should trigger downstream processing without waiting for the next scheduler run.

When webhook support is reliable, you get:

- Faster downstream posting

- Lower routine request volume

- Cleaner event-driven workflows

- Better user experience for near-real-time finance visibility

But webhooks come with more operational discipline. You need signature validation where supported, durable event ingestion, replay handling, idempotency protection, and dead-letter behavior for failures. You also can't assume event completeness. Some source systems emit create events but not all update or payout events you care about.

Use webhooks to learn that something changed. Use polling to confirm what the final state actually is.

That rule keeps developers out of a common trap. An order.add event is helpful, but it may arrive before payment, before tax finalization, or before a later correction. Finance records often need the durable state, not just the first event.

The hybrid model is usually the sane choice

For eCommerce finance, a hybrid design tends to hold up better in production.

| Pattern | Best fit | Main risk |

|---|---|---|

| Polling only | Batch import, reconciliation, uneven source event support | Delayed visibility |

| Webhooks only | Fast event awareness, reactive workflows | Missed or incomplete state |

| Hybrid | Event-driven triggers plus scheduled verification | More moving parts, but better control |

One practical pattern looks like this:

- Accept a webhook for order creation or update.

- Queue the store and order identifier.

- Fetch the full order from the source API before transforming.

- Post to the finance destination only after validation rules pass.

- Run scheduled polling to catch missed events and reconcile changed records.

For teams evaluating payment-adjacent workflow design, API2Cart's look at B2B payment automation integration patterns is relevant because it reflects the same architectural choice: event responsiveness is valuable, but finance-grade accuracy still needs verification.

This is also where a unified commerce API can be a strategic shortcut. API2Cart gives developers one integration layer for many carts and marketplaces, with both webhook support where available and list-based retrieval methods for polling and reconciliation. That matters less as a marketing claim than as an architectural simplifier. It reduces the number of sync models your team has to learn and maintain across platforms.

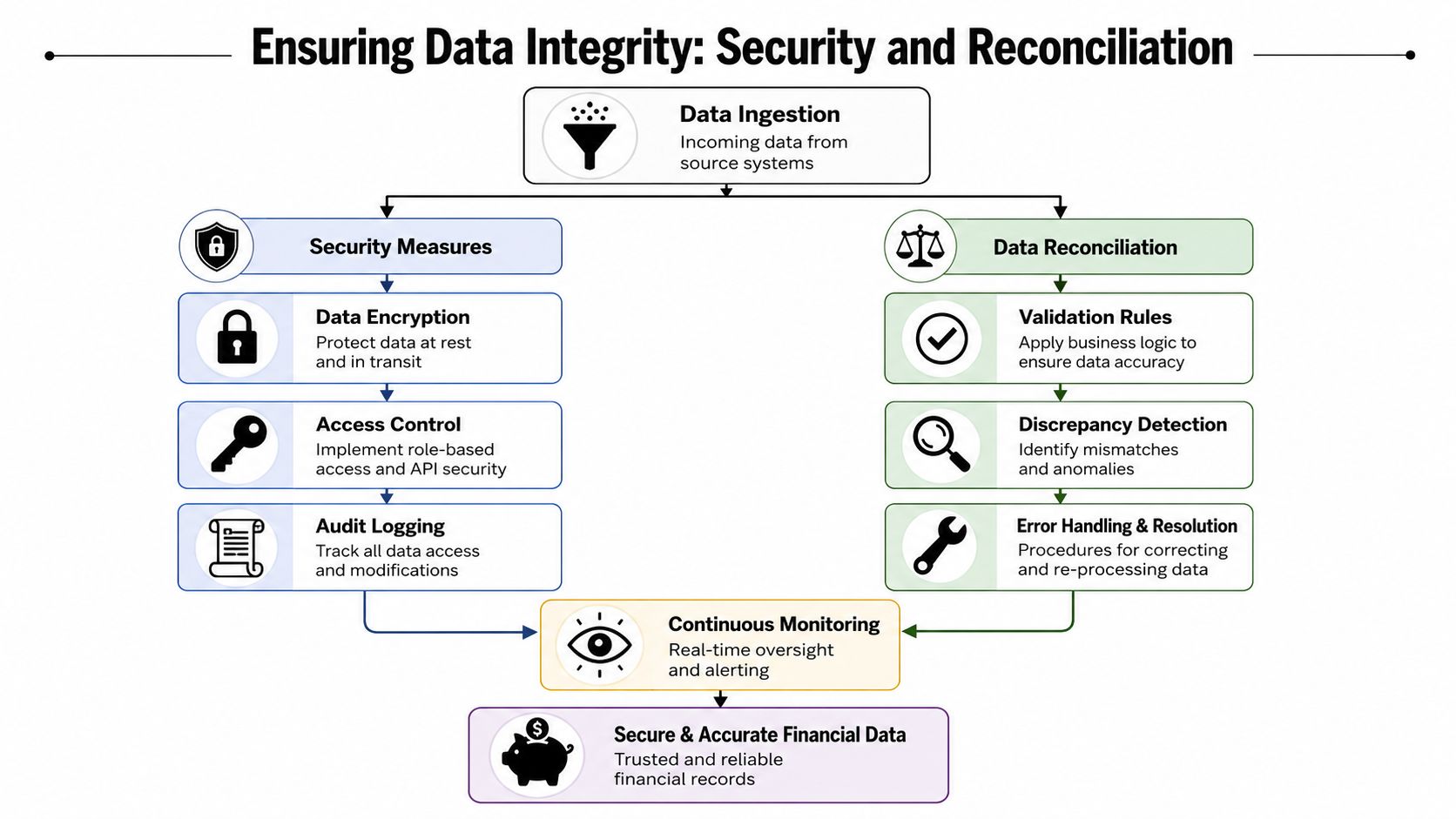

Ensuring Data Integrity Security and Reconciliation

Finance integrations fail in quieter ways than customer-facing features. A checkout bug gets noticed immediately. A tax mismatch or duplicate refund sync might sit in the ledger until month-end, when fixing it is more expensive and politically harder.

That's why security and reconciliation belong in the first release, not the cleanup phase.

A survey cited by Sprchrgr's finance integration analysis found that 48% of CFOs cite integration complexity as their top challenge, and 69% spend at least 5 hours per week on manual work that could be automated. For developers, that's a reminder that weak controls don't just create engineering debt. They create finance labor.

Lock down the connection surface

The basic security controls aren't optional.

- Limit credentials by purpose. Separate sandbox and production credentials. Don't let a testing workflow hold production access.

- Store secrets outside application code. Use a proper secret store and rotate on a schedule or after exposure risk.

- Apply least privilege. If the workflow only needs order and refund reads, don't request broader access than that.

- Encrypt in transit. Financial payloads should move over TLS-protected connections.

- Log access and write actions. You need a trail when finance asks who posted, retried, or changed a record.

The principle is simple. Every extra permission and every undocumented retry path becomes an audit problem later.

Reconciliation is the safety net

Reconciliation is the process that proves your integration is not drifting.

A practical daily routine often includes:

- Pull the count of source orders or updated orders for a defined period.

- Pull the detailed records for that same period.

- Sum the values your finance logic cares about, such as gross sales, tax, shipping, discounts, and refunds.

- Compare those values against what your destination system accepted.

- Flag mismatches for replay or manual review.

That process matters even if your sync looks clean. Commerce platforms can issue late updates. Destination systems can reject a transaction after your app marks it processed. A webhook can fail without notification if you don't persist the event correctly.

Reconciliation isn't a sign you don't trust the integration. It's the control that makes the integration trustworthy.

Build for duplicate prevention and traceability

Most finance data incidents boil down to four technical misses:

- No idempotency strategy, so retries create duplicate records

- Weak source references, so support can't trace a ledger entry back to the originating order

- Lossy transforms, so line-level tax or discount detail disappears

- No exception queue, so bad records fail invisibly

A simple traceability model helps. Store the source platform name, store identifier, source object ID, source updated timestamp, transformation version, destination record ID, and processing status for every finance event. That gives engineering and finance a shared record when something goes wrong.

If you want a practical merchant-facing complement to this architecture work, Shopify accounting tips from MetricMosaic, Inc. are useful because they frame the accounting side of the same data-quality problem your integration has to support. For a broader systems view, API2Cart's overview of banking system integration is also relevant because it highlights the same trust and data-flow concerns that show up in commerce-to-finance pipelines.

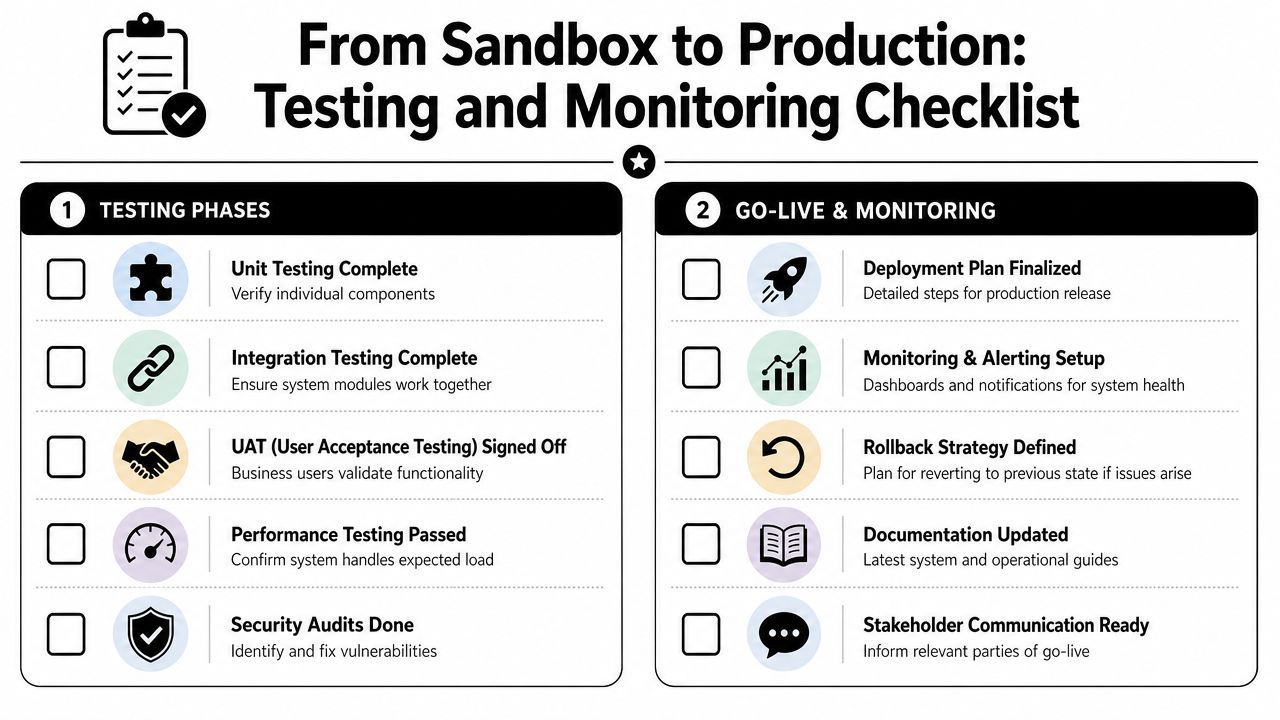

From Sandbox to Production Testing and Monitoring

A finance integration isn't ready when the happy path works. It's ready when bad payloads, duplicate events, delayed updates, and temporary destination failures behave predictably.

The safest rollout pattern is staged validation, then a controlled production release.

Test the mapping before you test the plumbing

Start with unit tests around transformation logic. Don't just test that an order imports. Test that a discounted multi-line order posts the expected line structure. Test partial refunds, order edits, canceled payments, tax-inclusive price models, and missing optional fields.

Then run end-to-end tests in a sandbox or isolated environment that mirrors production behavior as closely as possible. You want to verify:

- Input variability from different stores and channels

- Error handling when the source or destination returns incomplete data

- Retry behavior for transient failures

- Idempotency when the same event is delivered more than once

A lot of defects are really state-transition problems. The source says “created,” then “paid,” then “refunded,” and your code treats those as unrelated records. Testing needs to follow real sequence changes, not just single payload snapshots.

Parallel runs reduce go-live risk

Parallel validation is one of the most practical controls in finance integration. Instead of cutting over immediately, run the new integration alongside the current process and compare outputs before production becomes authoritative.

That approach aligns with the implementation sequencing described in the verified guidance around discovery, design, development, testing, parallel-run validation, and cutover in the earlier finance integration source. It's also how teams catch subtle differences in tax treatment, timing, or refund allocation before finance relies on the new feed.

During a parallel run, compare:

| Check | What to compare |

|---|---|

| Volume | Source order counts versus imported finance records |

| Value | Totals for sales, tax, shipping, discounts, refunds |

| Timing | Posting date versus expected accounting date |

| Exceptions | Rejected, skipped, or manually corrected records |

Monitor the integration like a product surface

Once live, the integration needs active monitoring. A “set it and forget it” posture is how small data issues become month-end fire drills.

Monitor at least these categories:

- API health. Request failures, timeout rates, and authentication problems.

- Sync latency. How long it takes for a source event to become a destination record.

- Webhook delivery failures. Missing acknowledgments, retries, and dead-letter growth.

- Reconciliation drift. Count and amount mismatches between source and destination.

- Exception backlog. Records waiting for manual review or replay.

The best production dashboard answers one question fast: which stores have financially incomplete data right now?

There's also a business side to testing and monitoring. NetSuite notes that teams often set targets such as reducing accounting close time by 50% during finance integration planning in its guide to finance integration. That's useful because it forces engineering to tie technical quality to an operational outcome, not just deployment success.

Avoiding Common Pitfalls in Finance Integration

Most finance integration failures are predictable. Teams just meet them in different orders.

The first pitfall is treating the project like a connector problem instead of a data-model problem. If you start from endpoints and not from finance outcomes, you'll ship something that moves data but doesn't produce reliable records.

The second is choosing one sync method dogmatically. Polling-only designs tend to frustrate users who need timely visibility. Webhook-only designs often break when event coverage is incomplete or state changes arrive out of order.

The third is postponing reconciliation. That decision usually happens because the initial demo worked, and everyone wants to move on. Then a few weeks later, support is trying to explain why source totals and destination totals don't line up.

Another common mistake is underestimating the non-technical side. The Aspen Institute notes that the hardest part of integration is often not the connection itself, but the surrounding infrastructure of trusted access, digital connectivity, and user education in its work on building inclusive financial systems. In a B2B SaaS setting, that translates to permissions, onboarding quality, operational ownership, and whether finance users trust the imported data.

A final trap is accepting long-term connector sprawl as normal. If your product roadmap depends on supporting many carts and marketplaces, every one-off integration adds maintenance burden, schema drift, and support complexity. That's manageable for a while, then it starts consuming roadmap capacity that should be going into product logic.

The better pattern is straightforward. Standardize the incoming commerce data shape as early as possible. Keep event handling and reconciliation separate. Preserve source references. Treat finance exceptions as first-class operational objects. And don't ship a “working” integration until support can trace a destination record back to the exact commerce event that created it.

If your team is building finance-facing eCommerce integrations and wants to avoid maintaining cart-specific connectors, API2Cart is worth evaluating. It gives developers a unified way to access store data across many platforms, which can simplify order, refund, tax, and customer-data ingestion for finance workflows. A free trial is the fastest way to validate whether its normalized access model fits your mapping, sync, and reconciliation requirements.